|

In June of 2012, the Consumer Financial Protection Bureau (CFPB) released a database of complaints submitted to the agency by credit card customers. Within the industry, this kind of information is known as "supervisory." For the last hundred years or so, it has been kept under wraps in the tidy confines of regulatory agencies. |

|

With the release of this database, the CFPB has placed a small nightlight in a very large, dark and messy closet. We can't really see what is going on in there, but the shadows may at least tell us what to be afraid of.

In March of 2013, the CFPB released an expanded version of the Consumer Complaint Database that includes complaints about mortgages, student loans, credit scores, and other products. The database houses information about more than 90,000 complaints lodged against the larger banks (i.e., those with more than $10 billion in assets). The complaints date from December 2011 to the present.

While the number of complaints seems impressive, the details are largely missing. A consumer can compare statistics on the raw number of complaints and other high level information, but this kind of data is not really very "actionable" in the traditional sense of the term. To understand why, let us take a look at what it started out as, what it offers to the public right now, and then consider what it could become.

In the past, a customer could submit a complaint to a financial institution, and perhaps send a copy to a regulatory agency such as the FDIC or the Office of the Comptroller of the Currency. The complaint was not made public, and if the response was less than satisfactory, the only option was to bring legal action against a defendant with very deep pockets and a much bigger hand in the legislative process. Few people found substantive justice.

The CFPB is chartered with a mission to mediate between the customer and a bank or other financial institution. Consumers may now submit complaints to the CFPB, which forwards them to banks and tracks the resolution. Early reports suggest the banks are responding a little faster and managing the complaints a little better these days. It's hard to tell from the data.

Let's take a peek at the database:

Like most database views, it doesn't fit in a browser window very well. Click the image above to view the sample in another window. Depending on your screen resolution and size, you may have to click the image in the new window to see it in full size (it should be legible, and you will probably have to scroll horizontally to see all the columns).

Notice that there are no low-level details. The columns, which have titles such as product, issue and company response, are used to present very high-level, abstract values.

For example, we can see that the Toyota Motor Credit Corporation received a complaint about a consumer loan (a vehicle lease), the zip code of the person who lodged the complaint, the date it was received by the CFPB and the date it was sent to the company. Other columns identify the response (closed with monetary relief, in this case) and whether or not the response was issued in a timely fashion. There is another column used to indicate if the consumer disputed the response.

The database offers the usual set of options to support analytic goals. Users can filter the data by product, company, issue, response, or any other column. Users can also export the data for use in Excel, Oracle or any other database application.

With a little work, a user may determine who is receiving the most complaints, or which zip codes are the source for the bulk of reports associated with a given issue. The capabilities are useful to the banks, which should use the data to address service issues in a far more proactive fashion. It is also useful to regulators: they may chart trends, assess where to focus their efforts and track results over time.

Customers, on the other hand, don't have much use for such abstract information. Let's take a look at the information presented for mortgages:

Click the image above to view the report in another window. Again, you may have to click the image in the new window to see it in full size (it should be legible, and you may have to scroll horizontally to see all the columns).

If a customer wanted to "vet" or perform due diligence on a bank before signing a mortgage, they could open the database, filter for a product (mortgage) and a company (PNC Bank) and, for example, find out how many complaints were lodged from their zip code. The issue categories, however, are very high-level and include the following:

- Loan Modification, Collection, Foreclosure

- Loan servicing, Payments, Escrow Account

- Credit Decision/Underwriting

- Settlement Process and Costs

- Application, Originator, Mortgage Broker

- Other

The Company Response entries are limited to the following:

- In Progress

- Closed with Explanation

- Closed with Monetary Relief

- Closed with Non-Monetary Relief

- Closed without Relief

- Closed

- Untimely Response

Two of the columns, Timely Response and Consumer Disputed, are limited to Yes/No indicators. The remaining fields are administrative: while the location information, submission channel and dates are useful for organizing the data, they don't offer much insight to a customer trying to make an informed decision. The number of complaints, 919 lodged between December of 2011 and April of 2013, does not offer a valuable metric on its own.

If a customer wanted to work really hard before signing off on a loan, they could review the 10-K and annual report content to gauge the financial health of the lender. Given the complexity of the information, and the numerous ways it is represented, not many of those who attempted the effort would find the evidence required to make a sound decision. After all, very few of the professional analysts foresaw the collapse of 2008 (and many of those who did were derided for their prescience).

We are left with a good question: what information would help a customer decide whether or not to do business with a bank or financial service provider?

Peeking under the scar tissue, and with the benefit of hindsight, we offer the following as a starting point:

- How many mortgages does this bank currently service?

919 out of how many customers lodged a complaint? - How many of this bank's mortgages ended in foreclosure last year?

Does this bank seek alternatives to foreclosure? - How many of this bank's mortgages ended in a short sale last year?

How many borrowers lost their entire investment? - How many loans were closed out due to a sale or loan payoff?

How many borrowers successfully ended a loan? (i.e., without a loss) - How many of the bank's loans are fixed rate? Variable rate?

Is this bank focused on traditional loans or higher risk activity? - What percentage of each payment is used for interest?

Does the bank publish amortization tables for its loans?

Working with the CFPB database, we can't answer any of these basic questions. In most cases, a banker would try to answer the questions listed above if they were asked by a prospective customer. If they will not, that may tell a prospective customer all they need to know about the company and its practices.

Perhaps the CFPB should set an explicit goal to find out which forms of information the consumer could use to make better decisions, and work with the banks to collect and publish the data in a form that is more actionable for the consumer.

In contrast, let us take a look at the kind of information about a prospective customer a bank may review before they make an offer:

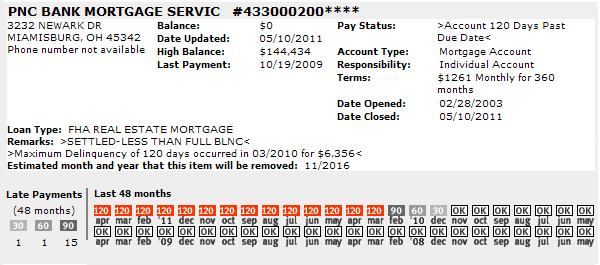

In a standard credit report, we find a person's name, address and phone number, a Social Security number, date of birth, prior addresses, a work history that may go back more than ten years, and gory details about any credit account opened in the last seven years.

The account information offers the name, address and phone number of each creditor, and low-level details that include the loan type, the balance, the high balance, the credit limit, the current pay status, the account type and terms, and the number of late payments, if any. For accounts with late payments, the report cites the "maximum delinquency" (i.e., how much was owed and how many days late the payment was).

The report also lists those who have requested and received copies. They also feature a graphic view of payment schedules with coded icons that call out which payments, if any, were missed. It's pretty much everything a bank can legally ask about a person before deciding whether or not to do business with them.

There is a lopsided or "asymmetric" quality to the nature of information used in the financial realm. While the banks can see all the cards an individual has played over the years, the customer can only wade through a sea of data and try to make some kind of informed guess about the hand a bank is holding very close to its vest.

The CFPB has an opportunity to even the odds for everyone by asking the right questions and expanding the database to place actionable information in the hands of consumers. Tell your story to the CFPB, and let them know which questions you would like answered before you decide to business with another bank.

Note: The larger banks have been pitching complaints about the CFPB database. The conventional argument asserts that by not collecting complaints about banks that have less than $10 billion in assets, the CFPB is "tilting" the playing field in their favor.

Given the advantages the larger banks enjoy, that's a bit like hearing the biggest bully on the playground complain about someone handing the little kids a whistle they can use to get the teacher's attention (or wake them up).

Don't buy into this self-serving rhetoric: the financial service industry better accept the fact that they have to play by the same rules as folks in any other service industry, especially if deregulation, a two-sided blade, will hold sway.

Print: |

|

|

|