As those who were covered by the Independent Foreclosure Review are aware, settlement checks sent to participants offered little more than a down payment on justice. In half the cases, a $300 check served as the punch line for a bad joke.

Following the review, the question is: What comes next?

We know the Senate Banking committee investigating the review uncovered some unpleasant facts. First, the banks defined the settlement amounts behind closed doors, and they aren't talking about how they did it or what criteria they used to reach their decisions.

We also know the agencies that managed the review have no plans to release any of the findings to consumers who are considering legal action. We are on our own, and many of us have started to discuss the possibility of a class action lawsuit.

In legal terms, those who lost a substantial amount of equity in a foreclosure may now submit a formal "request for disgorgement" to recover their share of the proceeds from a foreclosure or a short sale.

|

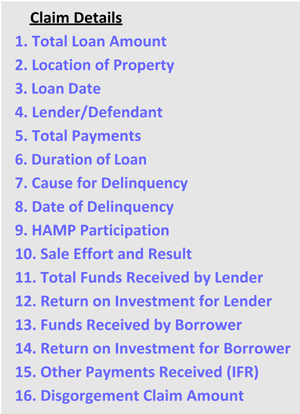

To begin the process, collect the facts of your case. The goal is to provide a judge with the details required to determine if you have a case for recovering a share of the equity held by a lender. To justify a claim, present the details in a clear, concise manner. Start with the facts of the loan: identify the amount, purpose, dates, and the name of the lender. Add up the total number and amount of payments you made, the number of months the loan was active, and tell the story of how the loan came to an end. State how much the lender received in payments, and in proceeds from the foreclosure or short sale. |

|

Then, use a ROI Calculator to determine how much the bank made from the loan. If the bank lost money on the loan; that is, if they did not recover the principal amount of the loan and a substantial profit in the form of interest, there is nothing to disgorge and you may not submit this kind of request. There may be other class action suits that are of interest, but you can't recover a fair share of profit if there is no profit. Refer to the formula below to see if you can play in this game:

To populate the formula ...

- Enter the total of all payments made for the loan

- Enter the total proceeds from a sale of foreclosure or a short sale

- Enter the sum of the payments and proceeds for a total revenue

- Subtract the amount of the loan from the total revenue

- Enter the difference between the revenue and the loan amount

- Calculate the return on investment the lender has retained

- Identify an amount that will constitute a fair return for the borrower

- Subtract the amount of disgorgement from the positive return

- Recalculate the return on investment for the lender

If you have a case, and a fair number for a judge to consider, the next step is to create a formal request for disgorgement. This simple document should present your case in no more than one thousand (1,000) words - about two standard pages. What follows are instructions for creating a request: feel free to draw from them, but recognize a lawyer may recommend different formats and strategies.

Start with a title and identification content:

Request for Disgorgement

Plaintiff: (Your Name)

Defendant: (Bank/Lender)

Loan (#0000000000)

Date: 05/01/2013

Enter your name, the bank or lender name, the loan number and the date.

Introduce the purpose of the request and the trigger for filing a case:

This is a formal request for disgorgement of profits associated with a loan made for a residential property. The loan in question was closed out in the aftermath of a "short sale" to the benefit of all involved except for the individual who took out the loan, the plaintiff.

Substitute "foreclosure" if appropriate.

Present a summary description of the legal argument:

The plaintiff in this request seeks to obtain the equity accrued over 6.5 years, which the defendant has claimed as profit. The plaintiff recognizes the defendant's right to recover the principal of the loan and a fair profit. What is at stake in this action is the defendant's claim to all proceeds from the short sale of the property securing the loan - i.e., that the plaintiff has no right to any share of the proceeds.

Identify the completed payment period for the loan (accrued over x years).

Establish the date of the loan, the lender, the amount of the loan, the property used to secure the loan, and the total amount of payments made against the loan over the payment period:

In March of 2003, the plaintiff secured a loan from National City Mortgage for $144,000 to purchase a property located at 103 Goldenrod in Bloomington, Illinois. Over a period of 6.5 years, the plaintiff paid more than $92,000 in monthly payments on this loan, and invested more than $10,000 in property improvements.

List the month and year that you took out the loan, name the bank and the principal amount, and identify the street address of the property. Provide the sum total of monthly payments and any other investments made in the property.

Describe any special conditions, and any participation in federal programs:

National City was purchased by PNC in October of 2008, and took over administration and ownership of the loan. As a result of the financial crisis of 2008, the plaintiff was laid off from a long-term, professional position in Bloomington, Illinois in July of 2009. The plaintiff applied for participation in the HAMP program immediately, and made several payments under this program between October and December of 2009, when PNC also began foreclosure proceedings (an example of so-called "dual-tracking").

Identify any questionable practices the lender engaged in.

Tell the story of how and why the loan ended:

In December of 2009, the plaintiff accepted a professional position in O'Fallon, Illinois, placed the house in Bloomington on the market at a fair market price ($159,000), and relocated to the St. Louis area. Over the following 14 months, the plaintiff did not receive any offers on the property, despite the best efforts of an experienced real estate agent.

In June of 2010, PNC Mortgage initiated foreclosure proceedings on the loan. The effort was complicated by an attempt to attach another debt collection effort to the proceeding. A foreclosure date was ultimately set for March of 2011. Approximately two weeks before the expected foreclosure date, a short-sale offer of $126,000 was made for the property. PNC Mortgage accepted the offer, and the sale was completed in April of 2011. The plaintiff received a $750 check following closure, and a negative entry on his credit report. PNC Mortgage kept all other proceeds from the sale, with the exception of fees collected by the real estate agents involved in the sale.

Define what drove the change, what happened, and how much money each party collected in the process of closing out the loan.

State your expectations and present the totals from the validation formula:

Given the nature of the property, and the local real estate market, the plaintiff expected to receive a normal and reasonable return on the investment.

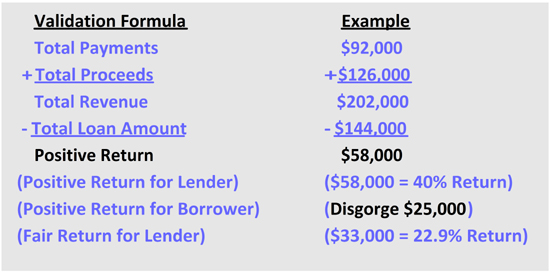

PNC Mortgage realized a return of $202,000 on a $144.000 loan over a period of eight years ($92,000 in payments and $110,000 in net proceeds from the sale). Their claim of interest, or net profit on the loan totals $58,000, less administrative costs. This represents a 40% gain on the investment, or a 4.3% annualized return.

The $750 the plaintiff received after the close of the sale represents the entire return on his $92,000 investment (a 99.2% loss). In April of 2013, the plaintiff also received a $2,000 check for participating in the Independent Foreclosure Review. The letter that accompanied the check does not offer a reason for the amount or any admission of wrongdoing on the part of the lender. The letter also indicates there is no process for appeal, which prompted the plaintiff to pursue this action.

Identify any other benefits received, including those received from the Independent Foreclosure Review and the remind the court that a) the banks set the amount of the check, and b) the agencies offered no process for appealing the settlement.

Present the substance of your argument and claim:

It is obvious the outcome of the loan is lopsided in favor of the defendant. As the findings of the Independent Foreclosure Review are not available for review, it is impossible to determine if the defendant violated any specific laws in the conduct of the transaction. The return on the investment for the defendant, however, appears to be a form of unjust enrichment given the specifics of this case. While the defendant is entitled to recover the principal of the loan in a short-sale transaction, and to retain a reasonable amount of profit, to keep all of the proceeds is patently unfair.

The plaintiff seeks a reasonable payment for the equity earned over eight years of investment. A sum of $25,000 is fair, and reasonable as it would allow the defendant a $33,000 net profit, a 22.9% gain on the investment (or a 2.6% annualized return). Such an award would provide the plaintiff with a "fair share" of the proceeds from the sale while allowing the defendant to make a reasonable profit.

Remind the court that the Independent Foreclosure Review offered no information to the consumers affected by the lender's practices, and this action is a civil matter (a D.A. or member of the Dept. of Justice would have to initiate criminal charges, which is not likely to happen). Clearly state your claim, and indicate how it would affect the defendent (i.e., how much profit they would retain).

Conclude your argument with salient points and limits to your claim:

As it stands, it appears that the defendant is using the plaintiff's equity to offset losses from other, more significant transactions. At the time the plaintiff placed the property on the market, there were at least ten other properties in the area that were originally valued at over $300,000 that were selling at around the same price as the plaintiff's property. While PNC may or may not have financed those homes, it is clear that practices in the banking industry created the market conditions that forced a short sale of the property used to secure the loan in question. The plaintiff understands that he must bear some of the loss associated with the market conditions, but it is not fair that the plaintiff must bear a complete loss so the defendant may realize a 40% gain on their investment.

Despite the eighteen month delay created by the Independent Foreclosure Review, and the considerable discomfort created by the total loss of equity, the plaintiff is not seeking any additional punitive damages. If the court seeks to include any additional fines or fees to help prevent future acts such as those described in this request, the plaintiff would not object.

Cover motives, larger contextual factors and limit the scope of your claim.

Templates |

Word |

OpenOffice |

Text |

After you have drafted a request, the next step is to file it in the CFPB Consumer Complaint Database. The Consumer Financial Protection Bureau (CFPB) will log your request, forward it to the lender, and track the response from the lender.

The lender may communicate with you and try to settle the matter outside of the courtroom. File the request with the CFPB to give that option a chance to work -- anytime we can spare the court from handling this type of issue, it is a better for everyone.

If a lender is serious about protecting their brand, and remaining in business, they will try to address your claim. If they don't respond, or offer to negotiate a settlement, the CFPB will track their activity and publish the result as part of their statistical profile of the lender. The first step, then, is giving the lender the chance to do the right thing while the CFPB watches. If the lender does not choose to settle the request directly, then the next steps will involve a court.

To submit the request, access the CFPB Consumer Complaint Database and select the Mortgage option.

On the first page of the form, copy and paste the description of what happened from your request into the text box. Reserve the section that has the substance of your argument and claim for the second page of the form. Select the "Problems when you are unable to pay" option for loan modification, collection, and foreclosure and select the type of loan from the menu (in many cases, a conventional fixed mortgage). Select the Continue option.

On the second page, copy and paste the substance of your argument and claim from your request into the online form. Select the Continue option. On the third page, enter your contact information, and select the Continue option.

On the fourth page, enter your loan number, the name of the lender and their address, and use the Attach option to include a copy of the formal request, along with any other documents you would like the CFPB to consider. Select the Continue option to access the Review page. Once submitted, the content of the form may not be edited - so carefully review all entries.

Watch for the "Property Address same as Mailing Address" option at the top of the fourth page (Product Information). It is selected by default: if you are no longer at the address (which is probably the case if you are attempting to recover equity), de-select the option and enter the address of the property used to secure the loan.

On the final page, select the legal disclaimer option ("The information given is true to the best of my knowledge and belief. I understand that the CFPB cannot act as my lawyer, a court of law, or a financial advisor") and select the Submit button to complete the process.

Be prepared to negotiate in good faith with the lender.

If the lender contacts you, listen closely, take notes, and hold your ground. With luck, you may be able to find a settlement that is fair.

More likely, you will receive a rote response and have to consider bringing an action against a lender in the court on your own, or seek others in a similar situation and consider joining a class-action lawsuit. It is still a little early in the game for class actions, but keep an eye out for those forming in your state. Actions at a national or federal level may take longer and may produce a smaller result.

Good Luck, and stay strong.

Print: |

|

|

|